Executive Summary

The central aim of this paper is to explore when investors should favor high-beta versus low-beta (or minimum volatility) equities, using an economic-regime lens to guide decision-making. By analyzing historical data and applying a rules-based framework, we demonstrate that a simple rotation strategy between high-beta and low-beta exposures can significantly improve portfolio outcomes compared to a static tilt toward either style.

Our core finding is straightforward yet powerful: investors are best served by tilting toward high-beta equities during Goldilocks regimes (characterized by accelerating growth and moderating inflation) and rotating into low-beta or minimum-volatility equities during Risk-Off regimes (defined by slowing growth combined with either rising or falling inflation). Historically, this regime-based switching improved risk-adjusted returns by producing both higher cumulative gains and lower drawdowns. From 1975 to 2025, this stylized rotation delivered an annualized active return of roughly +3.0% versus the global equity market, amounting to more than +328% in cumulative excess performance.

For practitioners, the guidance is pragmatic: keep a neutral core allocation, but allow for modest tilts (10–20%) toward high-beta in Goldilocks environments and toward low-beta in Risk-Off conditions. Such a framework can enhance upside capture in favorable conditions while preserving capital during turbulent periods.

1. Defining Economic Regimes

Understanding the relationship between beta exposures and the macroeconomic backdrop begins with defining the regimes themselves. We use an economic lens that simplifies the market environment into four archetypal regimes:

- Goldilocks (High Growth, Low Inflation): Growth is accelerating, GDP and corporate earnings revisions are trending upward, credit spreads are tightening, and yield curves are stable or steepening. Volatility is low or declining, and investor risk appetite is strong. These are periods where markets reward risk‑taking, with flows into equities, cyclicals, emerging markets, and credit.

- Heating Up (High Growth, Rising Inflation): Growth remains robust, but inflationary pressures are beginning to surface. Policy risk becomes more salient as central banks lean restrictive, volatility begins to creep higher, and the outlook becomes more uncertain. Investors remain engaged but start to moderate exposure.

- Slow Growth (Low Growth, Falling Inflation): Economic growth is deteriorating, earnings downgrades dominate, and disinflationary forces are evident. Policy may be easing, but defensive positioning takes hold. Volatility rises, credit spreads widen, and demand shifts toward quality.

- Stagflation (Low Growth, High Inflation): Perhaps the most challenging environment for risk assets, stagflation combines deteriorating growth with sticky inflation. Margins are pressured, real yields are elevated, and restrictive policy undermines valuations. Defensive sectors tend to lead as investors seek stability.

In practice, we classified regimes using a combination of simple proxies — the six‑month total return of the S&P 500 (as a growth signal) and the trend in six‑month realized volatility (as a proxy for inflation and risk). More sophisticated frameworks incorporate leading indicators such as the OECD Composite Leading Indicator (CLI) for growth and consumer price inflation (CPI) trends for inflation.

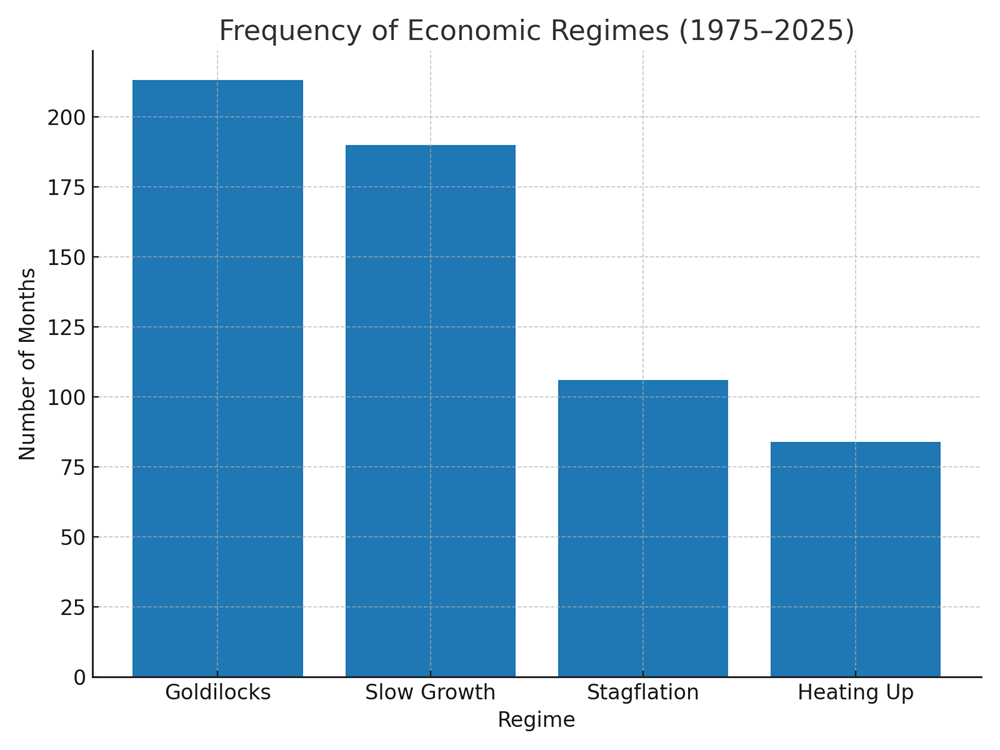

Figure 1: Frequency of economic regimes between 1975 and 2025. Goldilocks and Slow Growth were the most common environments.

2. Why High-Beta Works in Risk-On, and Low-Beta in Risk-Off

The economic rationale for rotating between high‑beta and low‑beta exposures is grounded in fundamental and behavioral dynamics.

In Risk‑On environments like Goldilocks, high‑beta stocks thrive. These companies often have greater operating and financial leverage, which amplifies earnings growth during expansions. Easy funding conditions, supportive credit markets, and falling volatility allow multiples to expand. Investor risk appetite further accelerates flows into cyclicals and growth‑sensitive sectors, rewarding high‑beta exposure.

In contrast, during Risk‑Off environments such as Slow Growth or Stagflation, low‑beta and minimum‑volatility equities shine. These companies typically operate in defensive industries such as utilities, healthcare, and consumer staples, where demand is inelastic. Their revenues are less sensitive to the business cycle, and their defensive appeal attracts flows when volatility rises. Empirically, low‑beta equities capture only about 50–70% of market drawdowns, making them effective shock absorbers.

3. Allocation Framework

To operationalize the insight, we developed a simple rules‑based allocation framework:

- Goldilocks (↑Growth, ↓Inflation): Overweight High Beta. Strong growth with benign inflation supports earnings leverage and risk appetite.

- Heating Up (↑Growth, ↑Inflation): Hold Market Neutral. Growth is intact, but rising inflation introduces policy risk and greater volatility.

- Slow Growth (↓Growth, ↓Inflation): Overweight Low Beta / Minimum Volatility. Defensive bias helps preserve capital during weak growth.

- Stagflation (↓Growth, ↑Inflation): Overweight Low Beta / Minimum Volatility. Sticky inflation and pressured margins lead investors toward defensives.

The trading rule is deliberately simple: if the economy is in Goldilocks, hold High‑Beta proxies; if in Slow Growth or Stagflation, hold Minimum Volatility proxies; if in Heating Up, remain neutral. To prevent look‑ahead bias, trades are executed with a one‑month lag after signal confirmation.

Figure 2: Average annualized excess returns of High Beta and Minimum Volatility equities across regimes.

4. Stylized Regime Study (1975–2025)

To test this framework, we conducted a stylized backtest across five decades of data. Between December 1975 and May 2025, the regimes occurred with the following frequencies: Goldilocks (213 months), Slow Growth (190), Stagflation (106), and Heating Up (84).

The results were striking:

- Minimum Volatility equities produced modest but consistent excess returns in Risk‑Off regimes (+0.3–0.4% per month).

- High Beta generated strong excess returns in Goldilocks (+2.6% annually, or roughly +0.2% per month).

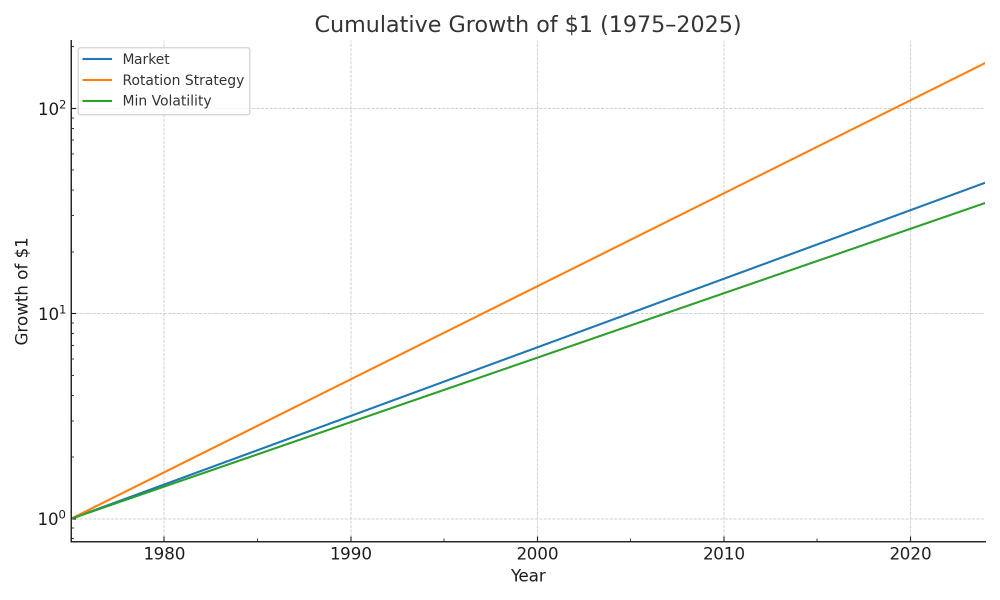

- The rotation strategy (High Beta in Goldilocks, Minimum Volatility in Risk‑Off, Market Neutral in Heating Up) delivered +2.98% per year in annualized active returns, amounting to +327.7% cumulative excess performance versus the global market.

- By contrast, a static Minimum Volatility allocation underperformed (−0.57% per year active), while holding the broad market produced zero active return by construction.

These results underscore a critical point: most of the historical opportunity was not in chasing outsized gains in Goldilocks alone, but in compounding the steady edge of Minimum Volatility during the majority of Risk‑Off months.

Figure 3: Cumulative growth of $1 invested in the market, rotation strategy, and static Minimum Volatility (1975–2025, log scale).

5. Implementation Guidance

While the backtest demonstrates clear potential, real‑world implementation requires discipline. We suggest the following considerations:

- Signal Construction: Use macroeconomic signals such as the OECD CLI for growth and CPI momentum for inflation. Supplement with PMIs, earnings revisions, credit spreads, and volatility term structure for robustness.

- Portfolio Design: Maintain a neutral strategic core allocation. Tilt 10–20% into High Beta during Goldilocks and Low Beta during Risk‑Off. Diversify further by adding Quality or Dividend factors in Risk‑Off, and Small‑Caps or Cyclicals in Goldilocks.

- Rebalancing: Implement monthly or quarterly rebalancing with a one‑month lag to reduce signal noise.

- Risk Controls: Set position limits, track tracking error, and consider volatility targeting (e.g., 8–12% annualized) to stabilize outcomes. Account for transaction costs and avoid excessive turnover.

6. Limitations and Next Steps

No model is without weaknesses. Regime detection is inherently noisy, particularly in real time. Signals such as CLI and CPI are revised and subject to lags, requiring smoothing and corroboration. Moreover, ETF histories are shorter than factor index data, which can limit backtest precision. Implementation costs, spreads, and taxes may erode returns if not carefully managed.

Future work could explore ensemble models that combine macro, market‑based, and earnings‑driven signals for regime classification. Additionally, optional overlays such as put options in Risk‑Off or call spreads in Goldilocks could provide convex payoffs and improve behavioral resilience for investors.

Conclusion

A compact regime‑aware approach to rotating between high‑beta and low‑beta equities offers a practical enhancement to traditional equity allocations. By tilting toward high‑beta during Goldilocks and low‑beta during Risk‑Off, investors can participate more fully in favorable conditions while defending better in adverse ones. The strategy has delivered meaningful historical outperformance and is supported by both fundamental rationale and empirical evidence.

Importantly, the approach is implementable within institutional or advisory workflows. With explicit growth‑inflation signals, prudent risk controls, and a disciplined tilt structure, investors can achieve not only stronger long‑term returns but also a more resilient and behaviorally sustainable investment journey.

Be More Confident About Retirement

No retiree stops needing income. And no retiree can know in advance which financial risks may threaten their standard-of-living.

Don't confront retirement without a plan for monthly income.

Jim Tassoni, founder of Armor Wealth Strategies, brings over two decades of financial expertise to guide clients towards clarity and certainty in their financial lives. Driven by his own life-changing experiences with a rare genetic condition, Jim is dedicated to helping others not only secure their financial future but also enjoy the life they have.

Reach out to Jim for a custom plan tailored to make the most of your financial and personal aspirations.